– Vatsal Rai

June 6, 2024

Introduction

In the ever-evolving landscape of U.S. tax laws, key components that greatly impact investment approaches are being closely reviewed and might face reform. The 1031 tax exchange is a primary focus of this scrutiny. A longstanding element of the Internal Revenue Code, the 1031 exchange is now under significant reconsideration. This analysis delves into the details of the 1031 exchange, often referred to as a “like-kind” exchange. This provision allows investors to defer capital gains taxes on real estate sales by reinvesting the proceeds into properties of a similar nature. Understanding the implications of potential changes to this provision is crucial for real estate investing strategies.

What is 1031 Exchange?

A 1031 exchange is a strategy used in real estate investing where investors can trade one investment property for another property of equal or greater value, thereby deferring the payment of capital gains taxes on the profit from the sale. This approach is particularly favored by investors who aim to enhance their property holdings without immediately incurring tax liabilities on the gains from their transactions. According to the FEA, approximately $100 billion in real estate assets were traded using 1031 exchanges in 2019. By using a 1031 exchange, investors can potentially increase their real estate portfolio, optimize their investment returns, and achieve long-term financial growth without the immediate tax burden that typically accompanies property sales. This is particularly relevant in light of ongoing discussions about tax reform and its potential impact on real estate investing.

Benefit for Investors

Opting for a 1031 exchange enables investors to reinvest the entire value of their property at the end of the holding period into a new property. This strategy enhances the potential for investment growth by deferring all taxes. Conversely, selling a property through a standard transaction incurs substantial tax liabilities, diminishing the funds available for reinvestment and, in turn, limiting future growth prospects. Therefore, a 1031 exchange is a more beneficial approach for investors aiming to amplify their real estate investments over time. By deferring taxes, it allows for the continued growth and compounding of their investment portfolio without the immediate burden of tax payments, providing a more efficient pathway to building wealth in real estate. This tax deferral mechanism plays a crucial role in real estate investing, especially in managing capital gain taxes.

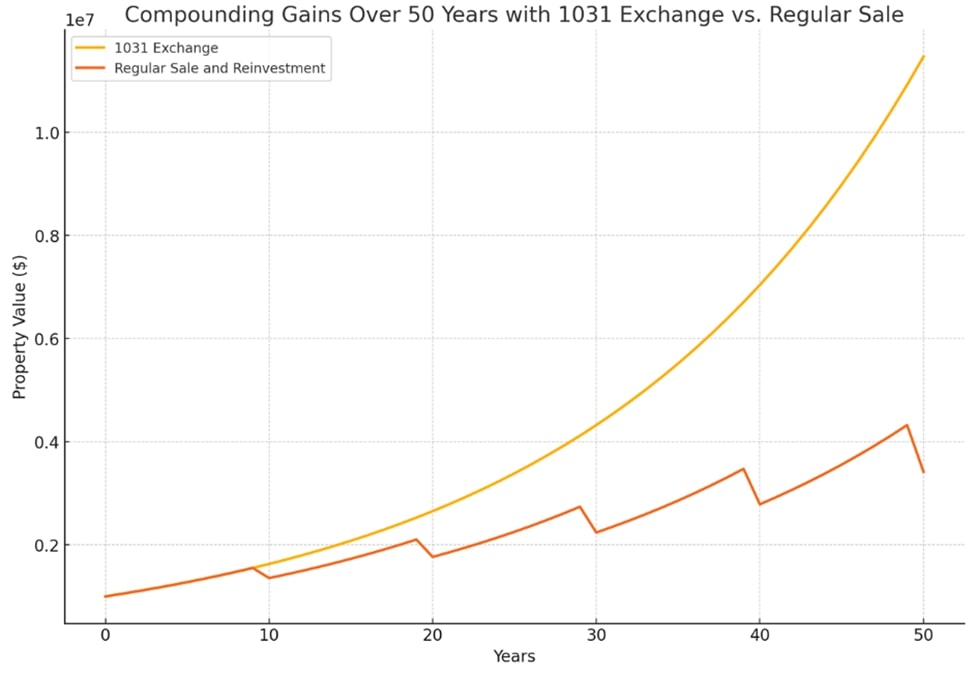

As illustrated in the below figure, there’s a significant difference between compounding gains with and without the 1031 exchange[1]

The 1031 Exchange line demonstrates a consistent, exponential growth pattern because the property’s full value appreciates without any reductions for taxes. On the other hand, the Regular Sale and Reinvestment line also exhibits growth, but with evident declines occurring every decade. These declines are attributed to taxes paid on gains and depreciation, which slightly diminish the effect of compounding over time.

The difference between the two lines highlights the impact of tax deferral in a 1031 Exchange. While the 1031 Exchange benefits from uninterrupted appreciation, the Regular Sale and Reinvestment approach faces periodic setbacks from taxation, which can erode some of the gains and slow down the overall growth trajectory. This comparison underscores the significant advantage of deferring taxes to maximize the property’s value and compounding benefits over the long term.

Biden Administration’s Proposal

In a bold and strategic decision, the Biden Administration has introduced a proposal aimed at eliminating the 1031 exchange, an integral part of its comprehensive tax reform agenda. This proposal seeks to generate additional revenue for government programs and to promote tax fairness by eliminating the ability to defer capital gains taxes on real estate transactions. The Biden administration contends that the proposed tax primarily affects affluent individuals and forecasts an increase of over 5 trillion dollars in the US economy over the next decade[4].

Advocates for this change believe it could address and correct persistent inequities within the tax system. Conversely, critics warn that this move might negatively impact real estate investors, disrupt the property market, and trigger broader economic repercussions. The debate highlights a significant tension between efforts to ensure a more equitable tax system and the potential risks to economic stability.

However, skeptics remain unconvinced. The Tax Foundation, an economic research organization, argues that the implementation of such a tax would have adverse effects in the long term, projecting a reduction of 220 basis points in the US GDP, a decrease of 160 basis points in wages, and the potential loss of over 700 thousand jobs.[4] Additionally, they assert that the new legislation would only contribute to the growing complexity of the US tax code. This complexity could pose additional challenges for those engaged in real estate investing.

Implications on Markets

Eliminating Tax-free exchange can have numerous implications on markets, as discussed below:

Impact on Real Estate Investment Strategies: If the 1031 tax exchange were eliminated, real estate investment strategies would experience significant transformations. Presently, this tax rule allows for the deferment of capital gains taxes when profits from property sales are reinvested in new properties. This mechanism maintains liquidity and enables investors to allocate more resources toward additional property purchases. Without it, investors would need to reconsider their approaches, as the immediate obligation to pay capital gains taxes would likely impact their financial flexibility and reduce their capacity for further investments.

Small vs. Large Investors: Data from a leading exchange facilitator indicates that the median sale price of properties involved in exchanges between 2010 and June 2020 was around $575,000.[3] This suggests that 1031 exchanges are widely utilized by a diverse range of taxpayers, encompassing various income levels and property values, rather than being dominated by large institutional investors. Hence, removing the 1031 tax exchange could significantly impact small and large investors differently. Small investors, who often have limited financial resources, rely heavily on the tax deferral provided by the 1031 exchange to buy properties and keep cash flow. Without this benefit, they might struggle to compete in the aggressive real estate market. On the other hand, large investors, with their substantial financial resources and access to capital, may be better equipped to handle this change. They could potentially use other strategies to mitigate the effects of immediate tax obligations.

Impact on Market Dynamics: The possible elimination of the 1031 tax exchange threatens to create major disruptions in the real estate market’s operations. Currently, this tax benefit fosters continuous reinvestment, contributing to market stability and encouraging investors to retain properties for longer periods. Removing this provision might lead investors to sell properties sooner than they would otherwise, potentially causing property values to fluctuate and disrupting established investment practices, which could introduce uncertainty and destabilize the market.

Implications on the US Economy

This policy has been instrumental in promoting ongoing investment within the real estate sector, contributing to a cycle of growth and prosperity. Should this provision be rescinded, there is a risk of a noticeable downturn in real estate transactions, potentially leading to weakened economic vitality across multiple sectors. The real estate industry is deeply interconnected with fields such as construction, finance, and professional services. The elimination of tax deferment could have adverse effects on these sectors, potentially resulting in job cuts and an overall economic slowdown. A comprehensive investigation on microeconomics, led by Professors Ling and Petrova, spanned two decades and analyzed 1.6 million properties. The findings suggest that any limitations or removal of Section 1031 would lead to a reduction in real estate transactions, an increase in capital costs, and a shrinkage in GDP. For instance, the removal of Section 1031 could potentially raise rental prices by approximately 6%.[5]

For investors, the possible elimination of the 1031 exchange presents significant financial hurdles. Currently, this policy allows for the postponement of capital gains taxes if the profits from the sale of an investment property are reinvested in a similar property within a specified timeframe. This arrangement encourages a continuous flow of capital and facilitates economic growth. Discontinuing this tax deferral option could escalate tax obligations for investors and diminish the incentive to reinvest, impacting their financial outcomes and profitability by increasing the tax burden.

Analysis of Counter Arguments

The debate over whether to eliminate the 1031 tax exchange encompasses a spectrum of perspectives. Advocates for its repeal emphasize the need for tax fairness and anticipate a boost in government revenue. They argue that the current system allows real estate investors to indefinitely defer paying capital gains taxes, resulting in significant loss of potential tax income. By abolishing the 1031 exchange, proponents aim to level the fiscal playing field for real estate investors.

However, despite the compelling case for ending the 1031 exchange, there are substantial counterarguments. Opponents warn of potential adverse effects on the economy and real estate market vitality. They express concerns about decreased investment activity if investors can no longer defer capital gains taxes through like-kind exchanges. This could lead to reduced market fluidity, lower property values, and hindered development efforts. Critics also highlight the disruption to the real estate market’s cyclical reinvestment pattern, which stimulates liquidity and transactional volume. Removing such tax provisions may disrupt this cycle, resulting in fewer property transactions, reduced liquidity, and impacting various sectors dependent on real estate activity.

Final Word

In conclusion, the potential elimination of the 1031 tax exchange by the Biden Administration carries significant implications for real estate investors and the broader economy. While proponents argue that this move would promote tax fairness and generate substantial government revenue, the consequences could be far-reaching and disruptive.

Critics contend that abolishing the 1031 exchange could impede investment activity, leading to reduced market liquidity, lower property values, and hindered development efforts. The real estate sector plays a pivotal role in driving economic growth, and any disruption to its cyclical reinvestment pattern could reverberate across multiple industries, potentially resulting in job losses and an overall economic slowdown. Furthermore, the impact on small investors should not be overlooked. Historically, the 1031 exchange has been utilized by a diverse range of taxpayers, not just large institutional investors. Removing this tax benefit could disproportionately affect small investors, who often rely on the tax deferral to maintain cash flow and remain competitive in the real estate market.

While the debate continues, it is essential to consider the potential ramifications carefully. A balanced approach that addresses concerns about tax fairness while minimizing disruptions to the real estate market and broader economy may be warranted. Policymakers must weigh the trade-offs between generating additional government revenue and preserving the mechanisms that facilitate investment, economic growth, and job creation. Ultimately, the decision to eliminate the 1031 tax exchange should be guided by a thorough understanding of its far-reaching implications, informed by input from various stakeholders and rigorous economic analysis. A measured and well-considered approach is crucial to ensure that any reforms promote long-term economic stability and equitable outcomes for all.