– Vatsal Rai

Introduction

Many income-focused funds utilize leverage – essentially borrowing money – to magnify their investment gains. While this method can yield substantial profits during periods of declining interest rates, it also exposes investors to considerable risks, particularly in environments where interest rates are on the rise. This piece delves into the disadvantages associated with leveraging in debt-focused funds and highlights the advantages of the Sortis Income Fund’s decision to avoid leverage, offering investors a safer alternative amidst current market condition.

Drawbacks of Leverage

Increased Risk: Leverage introduces a higher level of investment risks to income funds, which typically prioritize stability and consistent returns. By borrowing money to invest, the fund exposes itself to greater volatility in the market. While this can potentially lead to higher investment returns in favorable market conditions, it also amplifies losses during downturns, which may not align with the risk tolerance of income-oriented investors.

Interest Rate Sensitivity: Income funds often invest in fixed-income securities such as bonds, which are sensitive to changes in interest rates. If a leveraged income fund borrows money at a fixed rate and interest rates rise, the cost of borrowing increases. This can squeeze the fund’s returns, as the income generated by its fixed-income investments may not be sufficient to cover the higher interest expense, potentially leading to losses. For instance, the yield on the 10-year U.S. Treasury note began the year at 3.88%, climbing to a peak of 4.33% in February before easing slightly by month-end. Throughout the initial two months, it fluctuated between 3.90% and 4.30%. In contrast, it reached almost 5% in October 2023 due to changes in interest rates[1].

Income Stability: The primary objective of income funds is to provide investors with a stable and predictable stream of income. However, leverage introduces an element of uncertainty into this equation. The additional interest expense incurred through leverage can erode the fund’s income, reducing the amount available for distribution to investors. This undermines the fund’s ability to deliver on its income-focused mandate and complicates portfolio management.

Liquidity Risk: Leveraged income funds may face liquidity challenges, particularly during periods of market stress. In times of financial strain, leveraged funds tend to experience outflows averaging between approximately 0.7 to 1 percentage point higher than unleveraged funds, relative to their total net assets[8]. Moreover, the study[8] also indicates that investors in leveraged funds exhibit a heightened sensitivity to negative returns compared to those in unleveraged funds. When examining a flow-performance regression model, where past relative returns are interacted with fund leverage, we observe that outflows for leveraged funds surpass those for unleveraged funds by more than double.

If a significant number of investors decide to redeem their shares simultaneously, the fund may be forced to sell assets to meet redemption requests. However, selling assets under duress can lead to unfavorable prices, further exacerbating losses and potentially destabilizing the fund.

Regulatory Constraints: Regulatory bodies often impose limits on the amount of leverage that funds can employ to safeguard investors and maintain market stability. The Investment Company Act of 1940 restricts regulatory leverage to a maximum of 50% for preferred shares and 33 1/3% for debt, based on the overall assets of the fund at the time of issuance[2]. Exceeding these limits can result in regulatory sanctions or legal consequences for the fund manager. Therefore, leveraging beyond permissible levels not only exposes the fund to additional risk but also poses compliance and governance challenges.

Overall, while leverage has the potential to enhance returns, it also introduces significant risks that may not be suitable for income-focused investors. Careful consideration of these investment risks, along with an understanding of the fund’s investment strategy and objectives, is essential for investors evaluating leveraged income funds.

The Leverage Gamble

Leverage allows funds to invest more capital than they possess, thus magnifying potential gains. However, this double-edged sword also magnifies losses. Here’s how rising rates can negatively impact leveraged debt funds:

Decreasing Bond Prices: As interest rates rise, existing bonds with lower coupon rates become less attractive, leading to a decline in their market price. This price decline can significantly impact the fund’s net asset value (NAV), potentially eroding investor returns.

For instance, consider the scenario depicted in the table below: imagine a treasury bond with a 3% coupon rate. If, after a year, market interest rates decline to 2%, the bond will still maintain its 3% coupon rate, rendering it more valuable than newer bonds offering only a 2% coupon rate. Should you decide to sell the 3% bond before it matures, you’ll likely observe that its price has increased compared to a year earlier. However, alongside the price appreciation, the bond’s yield to maturity will decrease for prospective buyers purchasing it at the new, higher price[3].

| Financial Term | Today | 1 year later |

| Market Interest Rate | 3% | 2% |

| Coupon Rate (semi-annual payments) | 3% | 3% |

| Face Value | $1,000 | $1,000 |

| Maturity | 10 years | 9 years remaining |

| Price | $1,000 | $1,082 |

| Yield to Maturity | 3% | 2% |

Table 1 – If Market Interest Rates Decrease by One Percent[3]

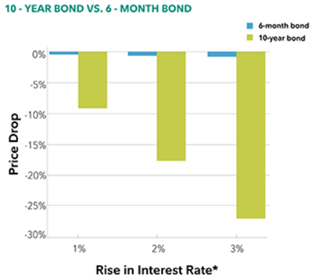

Margin Calls and Forced Selling: When bond prices fall due to rising rates, leveraged funds may face margin calls from lenders. To meet these calls, they may be forced to sell holdings at a loss, further amplifying the negative impact on NAV and investor returns. For example, the graph below demonstrates that a bond with a 5% annual coupon and a 10-year maturity (green bar) would experience a greater decline in price as interest rates increase, compared to a bond with a 5% coupon and a 6-month maturity (blue bar), primarily due to its longer duration[4].

Fig 1 – Price drops with interest rate increase [4]

Increased Borrowing Costs: Rising interest rates present a significant challenge for leveraged investment funds as they result in higher borrowing costs. These funds utilize borrowed capital to amplify their investment positions, aiming to magnify returns. However, when interest rates climb, the cost of borrowing rises correspondingly. This escalation in expenses directly erodes potential returns, diminishing the effectiveness of leverage as a wealth-building strategy. The ramifications of increased borrowing costs are particularly pronounced when combined with falling bond prices. As interest rates rise, bond prices tend to decline inversely. Leveraged investment funds, especially those heavily invested in fixed-income securities like bonds, face a double whammy: not only do they contend with the heightened expense of borrowing, but they also experience losses on their bond holdings.

Furthermore, the impact of rising borrowing costs extends beyond just reducing returns; it can potentially negate gains and even lead to losses for leveraged funds. In a scenario where interest rates rise swiftly or unexpectedly, leveraged funds may find themselves in a precarious position, struggling to generate positive returns amid mounting borrowing expenses and declining asset values.

Duration: Duration tends to increase when leverage is utilized. This is because leveraging amplifies a fund’s exposure to its portfolio assets. Consequently, funds employing leverage typically demonstrate heightened NAV and market price volatility compared to non-leveraged counterparts. Given their susceptibility to interest rate changes, leveraged funds may undergo more substantial NAV declines relative to similar unleveraged funds when interest rates rise. A decrease in NAV can lead to a corresponding reduction in the market price of the fund’s common stock. This also gives rise to Leverage Adjusted Duration, which is given by non-leveraged duration divided by non-leveraged percentage. For instance, if the actual duration is 5.5 years for a 30% levered fund, then the leverage adjusted duration will be 7.9 years[5].

The Sortis Advantage: Stability and Predictability

Sortis Investment Fund is an evergreen investment vehicle concentrated on procuring senior loans backed by real estate assets across the United States, particularly targeting Western US markets. SIF’s methodical investment strategy and stringent risk oversight yield a varied loan portfolio that offers investors stable, lucrative fixed-income returns, all achieved without resorting to leveraging. It focuses on an unleveraged mortgage fund that focuses on short-term, first position loans collateralized by commercial real estate[6].

Leveraging Sortis’ deep-rooted proficiency in real estate and banking, SIF strategically allocates capital in a landscape where traditional financial institutions fail to meet the burgeoning demand for financing. In the fiscal year 2022, it provided investors with a net return of 9.47%, steering clear of problematic asset classes while allocating capital to high-quality opportunities featuring value-driven business plans supported by seasoned operators. This approach aligns well with prudent portfolio management and sound investment strategy.

The Sortis Income Fund prioritizes capital preservation and consistent returns. By avoiding leverage, the fund sidesteps the risks outlined above. This approach offers several benefits:

Reduced Volatility: The unleveraged structure mitigates the price fluctuations experienced by leveraged funds during periods of rising rates, leading to a more stable investment experience for investors.

Protection of Principal: Leveraged funds, particularly those heavily invested in fixed-income securities, are susceptible to significant NAV declines when interest rates rise. As rates climb, the prices of existing bonds with lower coupon rates tend to fall, directly impacting the fund’s asset valuations. This effect is amplified for leveraged funds, as the borrowed capital used to magnify their positions exacerbates the impact of price movements on the overall NAV.

In contrast, the Sortis Income Fund’s unleveraged approach insulates it from this compounding effect. Without the burden of borrowed capital, the fund’s NAV is less exposed to the fluctuations in bond prices caused by interest rate changes. This safeguards the fund’s asset valuations, minimizing the risk of substantial NAV declines that could erode investor principal.

Attractive Returns: Despite the absence of leverage, the Sortis Income Fund aims to deliver competitive returns through careful security selection and active portfolio management. SIF produced a net annualized return of 9.86% during the fourth quarter of 2022[7].

Conclusion

The Sortis Income Fund presents a compelling alternative for income-oriented investors by consciously avoiding the use of leverage. This approach mitigates the risks commonly associated with leveraged funds, such as increased volatility, heightened interest rate sensitivity, and the potential for principal erosion. The unleveraged structure offers distinct advantages. It reduces exposure to the price fluctuations that leveraged funds often experience during periods of rising interest rates, leading to a more stable investment experience. Additionally, it prioritizes capital preservation by minimizing the risk of significant net asset value declines due to falling bond prices. Remarkably, despite forgoing leverage, SIF aims to deliver attractive returns through its disciplined security selection and active portfolio management strategies.

As the market navigates the challenges posed by rising interest rates and economic uncertainties, the Sortis Income Fund’s unwavering commitment to capital preservation and consistent returns positions it as a prudent choice. By sidestepping the pitfalls associated with leverage, the fund offers a stable and predictable approach to fixed-income investing, aligning with the risk tolerance of income-oriented investors while striving to generate attractive returns responsibly. This strategic approach ensures that the investment funds are managed with a keen eye on mitigating investment risks, optimizing investment returns, and adhering to a robust investment strategy.

References

[1] US Bank. 2021. “How Interest Rates Affect Bonds | U.S. Bank.” Www.usbank.com. July 7, 2021. https://www.usbank.com/investing/financial-perspectives/market-news/interest-rates-affect-bonds.html.

[2] Nuveen. 2020. “Understanding Leverage in Closed-End Funds.” Nuveen. Nuveen. August 4, 2020. https://www.nuveen.com/en-us/insights/closed-end-funds/understanding-leverage#:~:text=The%20amount%20of%20regulatory%20leverage.

[3] SEC. 2023. “Investor Bulletin Interest Rate Risk – When Interest Rates Go Up, Prices of Fixed-Rate Bonds Fall the Effect of Market Interest Rates on Bond Prices and Yield.” https://www.sec.gov/files/ib_interestraterisk.pdf.

[4] “Duration: Understanding the Relationship between Bond Prices and Interest Rates – Fidelity.” n.d. Www.fidelity.com. https://www.fidelity.com/learning-center/investment-products/fixed-income-bonds/duration.

[5] “Spotlight on Leverage in Closed-End Funds.” 2020. https://www.blackrock.com/us/individual/literature/investor-education/spotlight-leverage-cefs.pdf.

[6] “Sortis Income Fund.” n.d. Sortis Capital. Accessed March 26, 2024. https://sortis.com/income-fund/.

[7] wlcrmackenzie. 2023. “Sortis Income Fund Produces Net Annualized Return of 9.86% during Q4 of 2022.” Sortis Capital. February 1, 2023. https://sortis.com/blog/sortis-income-fund-produces-net-annualized-return-of-9-86-during-q4-of-2022/#:~:text=Sortis%20Income%20Fund%20Produces%20Net.

[8] Vivar, Luis Molestina, Michael Wedow, and Christian Weistroffer. “Burned by leverage? Flows and fragility in bond mutual funds.” Journal of Empirical Finance 72 (2023): 354-380.