– Vatsal Rai

April 8, 2024

Introduction

Private credit has swiftly emerged as one of the most compelling investment opportunities in recent years, offering investors avenues for financial stability and robust investment values. Once an overlooked corner of the financial markets, this alternative asset class now commands significant attention from investors seeking attractive returns, valuable diversification benefits, and the ability to structure customized financing solutions. As economic conditions evolve and market dynamics shift, private credit presents a unique opportunity to generate income, manage risk, and position portfolios for long-term success. With its potential to outperform traditional fixed-income investments and provide exposure to innovative lending strategies, private credit has solidified its place as a strategic component of the modern investor’s toolkit.

Growth of Private Credit

Private credit has swiftly emerged as one of the most compelling investment opportunities in recent years, offering investors avenues for financial stability and robust investment values. Once an overlooked corner of the financial markets, this alternative asset class now commands significant attention from investors seeking attractive returns, valuable diversification benefits, and the ability to structure customized financing solutions. As economic conditions evolve and market dynamics shift, private credit presents a unique opportunity to generate income, manage risk, and position portfolios for long-term success. With its potential to outperform traditional fixed-income investments and provide exposure to innovative lending strategies, private credit has solidified its place as a strategic component of the modern investor’s toolkit.

Growth of Private Credit

Following the 2008 financial crisis, there was a notable growth in private credit. As interest rates remained low, traditional investments like government and corporate bonds seemed less appealing to institutional investors and affluent individuals. This led to a trend dubbed “reach for yield,” where investors sought out riskier assets with higher returns, such as private credit funds.[7].

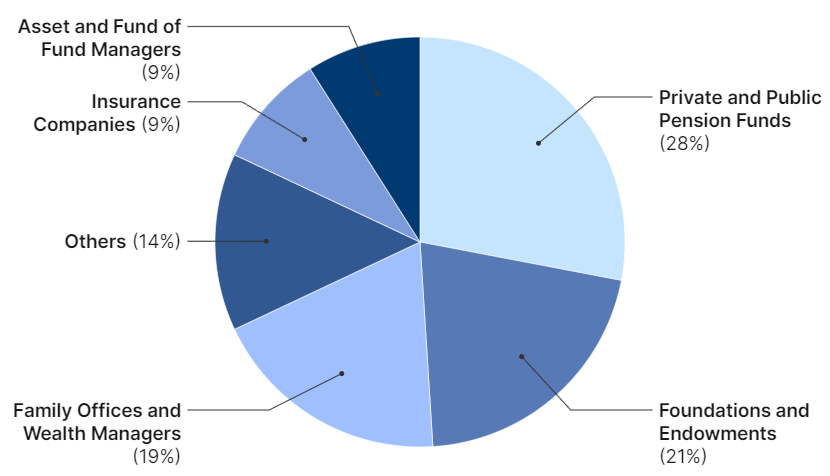

Fig – Investors in Private Credit[6]

According to an IMF report[6] based on data up to 2022, pension funds (28%), foundations and endowments (21%), and affluent families (19%) collectively contributed to over two-thirds of investments in U.S. private credit funds.

Size of Private Credit

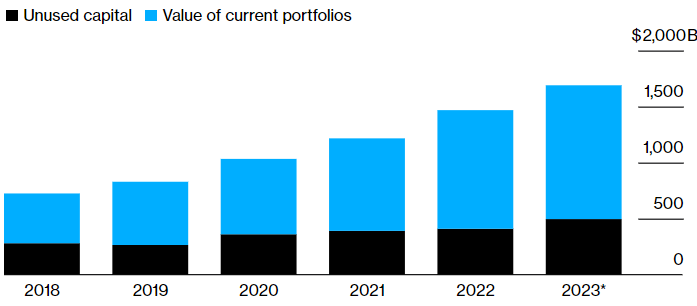

Private credit funds have capitalized on fluctuations in credit markets and instances where banks held unprofitable loans to expand their market presence. According to data from Preqin, closed-end private debt funds employing the five lending strategies mentioned above managed approximately $1.7 trillion in assets worldwide as of June 2023, a significant increase from about $500 billion in late 2015.[2] BlackRock Inc., a money management firm, forecasted in October that significant changes in financial markets would drive more borrowers towards private funds, potentially elevating the global private debt market’s value to $3.5 trillion by 2028.[3]

Fig 1 – Global AUM

Growth Drivers

The shift away from conventional lending avenues has prompted organizations to explore alternative funding channels in order to fuel their business expansion. Private credit emerges as a viable and expedient solution for these entities to procure the necessary capital.

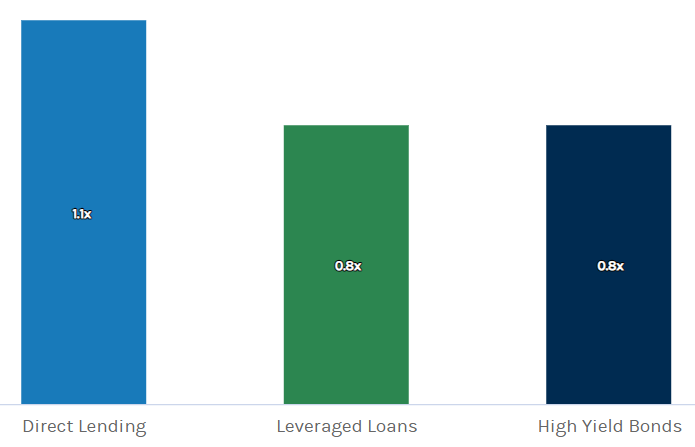

Moreover, investors exhibit a keen interest in private credit investment opportunities owing to their superior return rates compared to other investment vehicles. Highlighted by the Cliffwater Direct Lending Index for 2021, direct lending boasted an annual return rate of 9%, outperforming high-yield bonds at 8% and leveraged loans at 5%.[10]

Furthermore, the potential for increased interest rates presents an opportunity for investors to enhance their returns on investment. With many private credit loans featuring floating rates, they stand to benefit from rising interest rates. However, this scenario also amplifies the risk of lenders defaulting on their loans, underscoring the delicate balance between profitability and risk management in private credit investment.

Comparisons with traditional Asset classes

Throughout its history, private credit has shown impressive performance when compared to other sectors within the fixed-income market. Following the global financial crisis, private credit, particularly direct lending, has consistently delivered higher returns with less volatility compared to leveraged loans and high-yield bonds.[1]

Fig 2 – High Returns Relative to Volatility[1]

Moreover, private credit may provide enhanced safeguards against losses, as evidenced by its relative resilience during the COVID-19 pandemic. Between the onset of the pandemic and the second quarter of 2022, direct lending experienced losses of 1.2%, outperforming leveraged loans (1.4% losses) and high-yield bonds (2.7% losses).[1]

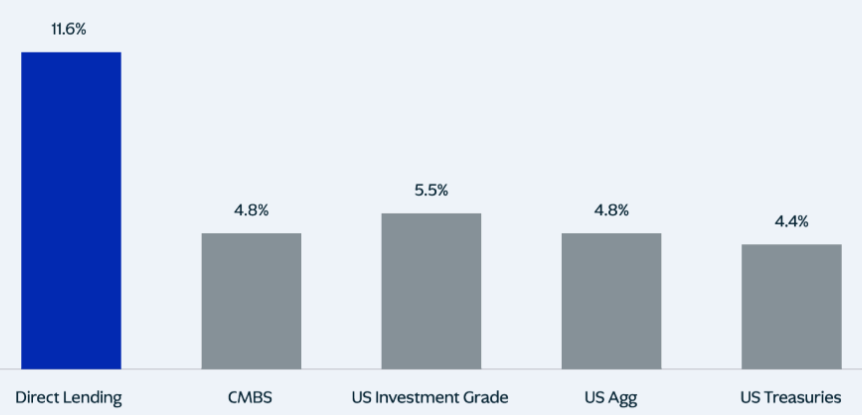

Private credit also has some of the highest Yield to Maturity among investment vehicles as shown below[5] which represents the overall return that balances the current market price of a loan with its expected interest payments and principal repayment at maturity. It’s important to note that this calculation assumes no losses from defaults, which may not be realistic, especially if loans are being traded at a discounted price.

Fig – YTM Comparisons [5]

Potential return enhancement and diversification

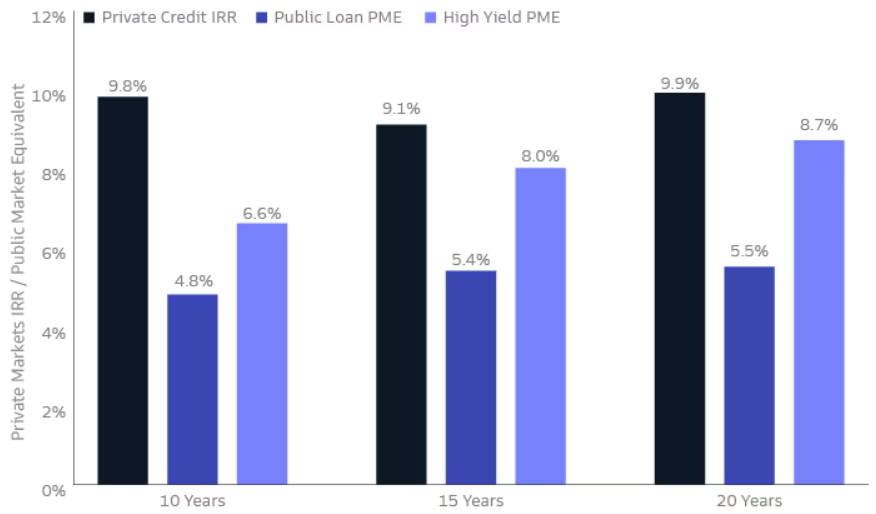

Assisted by the yield premium and its resilient nature, private credit has shown superior performance compared to public loans in the last decade, yielding annualized returns of 10% versus 5% for public loans. In an environment where interest rates are increasing, the floating rate characteristic of private credit could offer an additional advantage. Private credit instruments usually have ties to floating rates like SOFR. As interest rates go up, these increases are directly mirrored in the coupon of private credit, making floating-rate debt less susceptible to interest rate fluctuations in contrast to fixed-rate bonds, which typically decrease in value as interest rates climb.

Private credit also provides diversification benefits and can offer a hedge against market volatility. With concerns about economic uncertainty and market turbulence looming large, the ability of private credit to act as a portfolio stabilizer is a significant draw for family offices focused on preserving and growing their wealth. In an era of rising interest rates and market volatility, the income-generating potential of private credit strategies has become increasingly appealing to family offices seeking diversification and potential outperformance relative to traditional fixed-income investments.

Fig 3 – Comparison of overall performance [4]

Rising attractiveness among family offices

As family offices navigate an evolving investment landscape, private credit stands out as the most attractive option, offering avenues for financial stability and investment values. According to a recent Hedgeweek report, a remarkable six out of ten family offices plan to increase their exposure to private credit strategies in 2024, reflecting the growing recognition of its potential for financial stability and investment values while only 7% aim to reduce their allocations.[8]

This resounding endorsement of private credit reflects the unique advantages it offers in the current market environment. Private credit offers attractive risk-adjusted returns, especially in an environment where traditional fixed-income yields may be low. In an era of rising interest rates and market volatility, the income-generating potential of private credit strategies has become increasingly appealing to family offices seeking diversification. Beyond its attractive return profile and diversification benefits, the customizable nature of private credit strategies is also resonating with family offices. The ability to structure bespoke financing solutions also allows for better alignment with our investment objectives and risk appetite.

The surge in family office interest in private credit is part of a broader trend toward alternative investments. The Hedgeweek report[8] found that private equity (35%) and real estate (25%) are the next most popular asset classes among family offices, underscoring their appetite for strategies that offer potential return enhancement and portfolio diversification.

In contrast, traditional asset classes like equities (9%) and cash (2%) garnered relatively modest interest from family offices, reflecting a shift away from public markets and a desire for exposure to private market opportunities. Initial outperformance relative to traditional fixed-income investments.[9]

Conclusion

In the ever-evolving landscape of investment opportunities, private credit has emerged as a compelling force, attracting the attention of discerning investors worldwide. This alternative asset class offers a unique combination of attractive returns, valuable diversification benefits, and the ability to structure customized financing solutions tailored to specific investment goals.

As economic conditions fluctuate and market dynamics shift, the advantages of private credit become increasingly evident. Its resilience during periods of volatility and its potential to outperform traditional fixed-income investments position it as a strategic component of modern investment portfolios.

The growing interest from family offices, driven by evolving generational priorities and a desire for innovative investment approaches, further underscores the significance of private credit. As the wealth management industry continues to evolve, the role of private credit is poised to become even more prominent, presenting opportunities for investors to navigate uncertainty while pursuing long-term growth and stability.

By embracing the rise of private credit, investors can unlock a world of possibilities, combining attractive returns with valuable risk management tools and the ability to align investments with their unique objectives and values. The future of private credit is undoubtedly bright, and its ascent is set to reshape the investment landscape for years to come.

References

[1] “Outlook: Private Credit | Morgan Stanley.” 2023. Morgan Stanley. Morgan Stanley. 2023. https://www.morganstanley.com/ideas/private-credit-outlook-considerations.

[2] “Bloomberg – Are You a Robot?” n.d. Www.bloomberg.com. https://www.bloomberg.com/news/articles/2024-02-20/what-is-private-credit-how-does-it-work-and-what-are-the-risks.

[3] “The Nuances of Private Debt – Institutional.” n.d. BlackRock. Accessed April 6, 2024. https://www.blackrock.com/institutions/en-us/insights/private-debt-exploring-the-nuances.

[4] “Understanding Private Credit”. GSAM Insights. 2022.

https://www.gsam.com/content/gsam/us/en/advisors/market-insights/gsam-insights/2022/understanding-private-credit.html

[5] KKR. (2023). Private Credit Investing: What You Need to Know. [online] Available at: https://www.kkr.com/alternatives-unlocked/private-credit [Accessed 6 Apr. 2024].

[6] IMF. 2023. “Global Financial Stability Report, April 2023.” IMF. 2023. https://www.imf.org/en/Publications/GFSR/Issues/2023/04/11/global-financial-stability-report-april-2023.

[7] “What Is Private Credit? Does It Pose Financial Stability Risks?” n.d. Brookings. https://www.brookings.edu/articles/what-is-private-credit-does-it-pose-financial-stability-risks/.

[8] “Hedgeweek Insight Report – Family Offices: A New Era of Growth.” n.d. Resources.hedgeweek.com. Accessed April 6, 2024. https://resources.hedgeweek.com/family-offices?registration_source=hw_site.

[9] Craincurrency. 2024. “Survey: Private credit most attractive asset class for family offices” https://www.craincurrency.com/investing/private-credit-most-attractive-asset-class-family-offices-survey?utm_content=288082833&utm_medium=social&utm_source=linkedin&hss_channel=lis-UkdVNhDRzP

[10] Bartel, Jeffrey. n.d. “Council Post: Private Credit Investing: Current Opportunities and Risks.” Forbes. Accessed April 6, 2024. https://www.forbes.com/sites/forbesfinancecouncil/2023/03/30/private-credit-investing-current-opportunities-and-risks/?sh=4b2e10b23821.