-Shekhar Tripathi

April 30, 2024

Introduction

In an era marked by unprecedented economic upheavals, geopolitical tensions, and disruptive technological advancements, the conventional approaches to wealth preservation and growth have been put to the test. The global financial crisis of 2008, followed by bouts of market volatility and prolonged low-interest rate environments, exposed the vulnerabilities of relying solely on traditional investment vehicles. Family offices, entrusted with safeguarding and propagating multi-generational wealth, have found themselves at a crossroads, compelled to reevaluate their investment strategies and explore new frontiers beyond the realms of public equities and bonds.

This catalyst for change has led many family offices to turn their attention towards the burgeoning world of private credit, an alternative investment class that promises to fortify their portfolios against the tides of uncertainty while unlocking new avenues for potential returns. By allocating a strategic portion of their assets to private credit, family offices can tap into a diverse array of investment opportunities that exhibit low correlations with traditional asset classes, mitigating overall portfolio risk and potentially enhancing returns. Private credit can offer floating interest rates that increase in tandem with benchmark rates, has seen significant growth in recent years, and could become a $2.3 trillion market by 2027(1).

Understanding Private Credit: A Primer

Private credit encompasses a broad range of non-bank lending activities, including direct lending, mezzanine financing, distressed debt, and special situation investments. This asset class provides capital to companies that may not have access to traditional financing sources, such as bank loans or public debt markets. In return, private credit investors can earn attractive risk-adjusted returns, often in the form of cash flows from interest payments and potential equity upside.

One of the key advantages of private credit is its low correlation with public markets(1). As private credit investments are not directly tied to the ebbs and flows of the stock and bond markets, they can provide a valuable source of diversification for family office portfolios. According to a study by Preqin, the correlation between private credit and global equities has historically been around 0.3, indicating a relatively low level of interdependence.[1]

Furthermore, private credit investments offer the potential for higher returns compared to traditional fixed-income instruments. For instance, direct lending strategies, which involve providing loans to middle-market companies, have historically generated net returns in the range of 8% to 12%, significantly outperforming investment-grade corporate bonds.(2) Last year’s performance was solid overall, with the Cliffwater Direct Lending Index(3) clocking a total return of 12% in 2023. Also, J.P. Morgan Asset Management’s 2024 Long-Term Capital Market Assumptions (LTCMAs) suggest that direct lending would likely deliver annual total returns in excess of 8.5% over the next decade.(3)

The Allure of Private Credit for Family Offices

Family offices have emerged as prominent players in the private credit space, with six in ten planning to increase their investments in this asset class by 2024.(4) This shift is driven by the asset class’s unique characteristics and potential benefits. Unlike traditional investment vehicles, private credit offers family offices the opportunity to tap into a wide range of investment strategies tailored to their specific risk-return profiles and investment horizons.

One of the key advantages of private credit for family offices is the potential for enhanced portfolio diversification. By allocating a portion of their assets to private credit strategies, family offices can reduce their overall portfolio risk while maintaining the potential for attractive returns. This diversification benefit is particularly appealing for family offices with substantial holdings in public markets, as it can help mitigate the impact of market downturns on their portfolios.

Moreover, private credit investments often provide family offices with a steady stream of income, a valuable feature for those seeking to maintain a consistent cash flow. This income can be reinvested or used to fund various family office initiatives, such as philanthropic endeavors or entrepreneurial ventures.

Another compelling aspect of private credit for family offices is the potential for active involvement in the investment process. Unlike passive investments in public markets, private credit strategies often involve direct negotiations with borrowers, enabling family offices to exert influence over investment terms and conditions. This level of control can be particularly appealing for family offices seeking to align their investments with their values and investment philosophies.

The Spectrum of Private Credit Opportunities

The private credit landscape is vast and diverse, offering family offices a wide array of investment strategies to explore. Each strategy carries its own unique risk-return profile, liquidity characteristics, and potential benefits, allowing family offices to tailor their exposures to their specific investment objectives.

1. Direct Lending:

Direct lending represents one of the most prominent segments of the private credit market. In this strategy, investors provide loans directly to middle-market companies, bypassing traditional banking intermediaries. These loans can take various forms, including senior secured loans, unitranche facilities, and mezzanine financing.

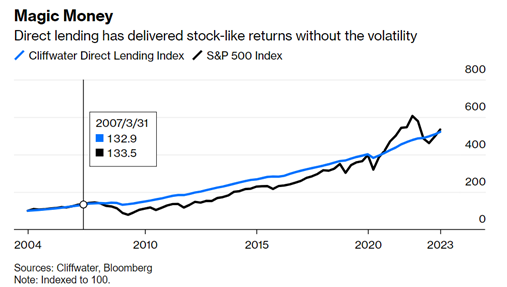

Direct lending strategies have gained popularity among family offices due to their potential for attractive risk-adjusted returns and steady cash flows and low volatility. Performance results for direct lending are scarce because private loans are not publicly traded, but the available data explains why it’s so popular. The Cliffwater Direct Lending Index, a collection of more than 12,000 middle-market loans, shows a return of 9.3% a year since 2004, nearly matching the S&P 500 Index’s return of 9.5% during the same period.(5)

The astonishing part is that direct lending has kept pace with stocks while looking more like cash. The direct-lending index’s volatility, as measured by annualized standard deviation, has been 3.5% since inception, which is a lot closer to the volatility of Treasury bills (0.8%) than the S&P 500 (16.2%) over the same time.(5)

2. Distressed Debt and Special Situations:

Distressed debt and special situations investing involve acquiring the debt of companies facing financial difficulties or undergoing restructuring. These investments can take the form of loans, bonds, or other debt instruments, often purchased at a discount to their face value.

While these strategies carry higher risk due to the distressed nature of the underlying companies, they also offer the potential for significant upside if the companies successfully restructure or turn around their operations. Family offices with a higher risk appetite and longer investment horizons may find these opportunities appealing.

3. Mezzanine Financing:

Mezzanine financing occupies a middle ground between equity and debt financing. In this strategy, investors provide subordinated debt or preferred equity to companies, typically in conjunction with a senior debt facility. Mezzanine financing is often used to fund acquisitions, expansions, or other growth initiatives.

For family offices, mezzanine financing can provide an attractive combination of current income through interest payments and potential equity upside if the company performs well. This hybrid structure can offer a balanced risk-return profile, appealing to family offices seeking a blend of income and capital appreciation.

4. Venture Debt:

Venture debt involves providing loans to early-stage or growth-stage companies, often in the technology or life sciences sectors. These loans are typically used to fund working capital needs, product development, or other operational expenses.

While venture debt carries higher risk due to the inherent uncertainties associated with early-stage companies, it also offers the potential for significant returns if the underlying companies achieve success. Family offices with an appetite for riskier investments and a long-term perspective may find venture debt an attractive complement to their existing venture capital or private equity portfolios.

The diverse range of private credit strategies available allows family offices to construct customized portfolios that align with their risk tolerance, return objectives, and liquidity needs. By carefully allocating capital across these various strategies, family offices can enhance their overall portfolio diversification and potentially improve their risk-adjusted returns.

Associated Risks & Challenges

While private credit presents compelling opportunities for portfolio diversification and potential returns, it is essential for family offices to understand and manage the associated risks and challenges carefully. Prudent risk management is crucial to ensuring the long-term success of private credit investments and preserving intergenerational wealth.

1. Liquidity and Lock-up Periods:

One of the primary challenges associated with private credit investments is their illiquid nature. Unlike publicly traded securities, private credit investments typically have lock-up periods ranging from several years to over a decade. This lack of liquidity can pose challenges for family offices in need of immediate access to capital.(7)

To mitigate this risk, family offices should carefully assess their liquidity needs and cashflow requirements before allocating capital to private credit strategies. Additionally, they may consider structuring their private credit portfolios with staggered investment periods or exploring more liquid strategies, such as direct lending funds with shorter lock-up periods.

2. Default Risk and Credit Analysis:

Nevertheless, year-to-date default rates have generally been low (figure below), compared to the broadly syndicated loan market or HY bond market, particularly in direct lending. However, private credit investments are inherently exposed to the risk of borrower default. Unlike public debt markets, where credit ratings and extensive research coverage are available, private credit investments often require thorough due diligence and credit analysis by the investor.

Family offices should invest considerable resources in developing robust credit analysis capabilities or partner with experienced private credit managers with proven track records in credit underwriting. Comprehensive due diligence, including financial statement analysis, industry research, and management assessments, is crucial to mitigating default risk.

Year-to-Date Default Rate (As of Oct, 2023)

(Source: KBRA DLD)

3. Operational and Legal Complexities:

Private credit investments can be operationally and legally complex, involving intricate deal structures, extensive documentation, and specific regulatory considerations. Family offices may need to navigate various legal and tax implications, including those related to structuring, domiciling, and reporting requirements.

To address these complexities, family offices should consider building in-house expertise or partnering with experienced legal and tax advisors specializing in private credit investments. Additionally, outsourcing certain operational functions to specialized service providers can help streamline processes and ensure compliance with relevant regulations.

4. Concentration Risk:

Given the idiosyncratic nature of private credit investments, family offices may face concentration risks if their portfolios are overly exposed to specific industries, geographies, or borrower types. Excessive concentration can amplify portfolio risk and potentially undermine the diversification benefits sought through private credit investments.

To mitigate concentration risk, family offices should strive to construct well-diversified private credit portfolios spanning various strategies, sectors, and geographic regions. Regular portfolio monitoring and rebalancing may be necessary to maintain optimal diversification levels.

By proactively managing these risks and challenges, family offices can position themselves to capitalize on the potential benefits of private credit investments while safeguarding their long-term financial objectives. Partnering with experienced private credit managers, leveraging robust due diligence processes, and maintaining a disciplined approach to risk management are critical components of a successful private credit investment strategy.

Navigating the Private Credit Landscape

As family offices explore the world of private credit, they have several options for accessing these investment opportunities. Each approach carries its own set of advantages and considerations, and the optimal choice will depend on the family office’s specific circumstances, resources, and objectives.

1. Direct Investments:

Family offices with substantial in-house expertise and resources may choose to pursue direct investments in private credit opportunities. This approach involves sourcing, evaluating, and negotiating deals directly with borrowers, as well as managing the investments throughout their lifecycle.

Direct investments offer family offices greater control over the investment process and the potential for higher returns by eliminating the fees associated with fund structures. However, this approach also requires significant investment in building a dedicated team with expertise in credit analysis, legal and regulatory compliance, and portfolio management.

2. Partnering with Private Credit Funds:

For many family offices, partnering with established private credit fund managers may be a more practical and efficient route to accessing private credit investments. These fund managers specialize in various private credit strategies, leveraging their extensive networks, investment expertise, and operational capabilities.

By investing in private credit funds, family offices can gain exposure to a diversified portfolio of private credit investments while benefiting from the fund manager’s due diligence, risk management, and portfolio construction processes. This approach can be particularly attractive for family offices with limited in-house resources or those seeking to diversify their existing private credit exposures.

3. Co-Investments and Direct Deals:

In addition to fund investments, some family offices may explore co-investment opportunities or direct deals alongside experienced private credit managers. Co-investments allow family offices to invest directly in specific transactions alongside the fund manager, potentially offering more favorable economics and increased control over the investment process.

Direct deals, on the other hand, involve family offices sourcing and executing private credit transactions independently, often in collaboration with other investors or borrowers. These opportunities can provide family offices with greater flexibility and customization but require substantial in-house expertise and resources.

Selecting the Right Approach

The optimal approach to accessing private credit investments will depend on the family office’s specific goals, resources, and risk tolerance. Family offices with significant in-house capabilities and a desire for greater control may prefer direct investments or co-investments, while those seeking diversification and access to specialized expertise may find partnering with private credit funds more advantageous.

Regardless of the chosen approach, conducting thorough due diligence on potential investment partners, fund managers, or direct investment opportunities is paramount. Family offices should carefully evaluate factors such as track record, investment philosophy, risk management processes, and alignment of interests.

By navigating the private credit landscape strategically and aligning their investment approach with their objectives and resources, family offices can effectively leverage the potential benefits of private credit investments in enhancing their portfolio diversification and achieving their long-term financial goals.

One compelling option for investors is the Sortis Income Fund (SIF), an evergreen, unleveraged private credit fund focused on senior secured loans backed by commercial real estate collateral in the Western United States. With over 7 years of successful operations, SIF has demonstrated a strong track record of preserving principal and generating attractive risk-adjusted returns with over 28 consecutive profitable quarters, distributing over $40 million to investors to date. By leveraging the team’s extensive experience of over 30+ years in real estate investment, development, and asset management, SIF employs a disciplined underwriting approach and tailored loan structuring to meet the specific needs of borrowers while prioritizing downside protection for investors. Additionally, Sortis offers the Sortis Edge platform, providing access to a diverse range of alternative investment opportunities beyond private credit. With a focus on identifying emerging trends and capitalizing on market inefficiencies, Sortis Edge allows investors to diversify their portfolios across a spectrum of alternative asset classes, further enhancing their potential for risk-adjusted returns. Learn more about Sortis here.

References:

[1] Morgan Stanley. (2023). Understanding Private Credit

[2] Taylor and Francis Online. (2024). Direct Lending: Benefits, Risks and Opportunities.

https://www.tandfonline.com/doi/full/10.1080/0015198X.2023.2254199#:~:text

[3] JP Morgan. (2024). Four Reasons to Consider Private Credit Despite The Headlines

[4] Flavio Moretto. (2024). Family Offices’ Pivot to Private Credit https://www.linkedin.com/pulse/family-offices-pivot-private-credit-flavio-moretto-5z7vf

[5] Bloomberg. (2023). Looks Like Cash and Acts Like Stocks, But It Has a Catch

[6] Cliffwater LLC. (2024). Study on Private Fund Fees and Expenses for Direct Lending

https://www.cliffwater.com/Resources

[7] Federal Reserve. (2024). Private Credit: Characteristics and Risks