– Vatsal Rai

April 17, 2024

Introduction

Inflation, the persistent increase in the prices of goods and services, poses a significant threat to the purchasing power of one’s retirement savings. As the cost of living rises, the value of money diminishes over time. While maintaining a diversified investment portfolio, including stocks, bond investments, commodities, and real estate, can provide some degree of protection against this risk, it’s essential to recognize that certain asset classes offer more robust defenses against the erosive effects of inflation.

Diversification across various asset types is a prudent strategy to mitigate the impact of inflation on your financial well-being, enhancing investment returns and risk mitigation. Bond investments, for instance, can offer stable income streams and are often considered lower risk compared to stocks. Let’s explore some of the most effective hedges and understand how they can protect your financial future.

Gold: A Timeless Safe Haven

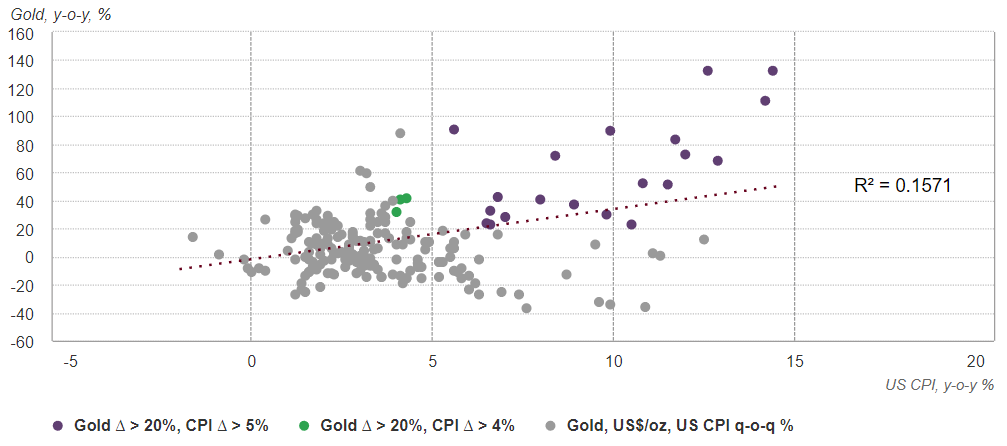

Fig. 1 – Correlation between % y-o-y change in gold US$ and US CPI [1]

For centuries, gold has been a symbol of wealth and stability. Its scarcity and historical lack of correlation with traditional investments make it a popular choice for inflation protection. During inflationary periods, the price of gold tends to rise alongside other commodities, acting as a hedge against a weakening currency and enhancing investment returns. The above chart shows a weak correlation between gold and % y-o-y change in gold US$ and US CPI, indicating that investing in gold is a good bet against inflation as it is not affected by rising prices. Indeed, it’s noteworthy that from the early 1980s onward, there was only one prolonged period characterized by ‘uncomfortably’ high CPI inflation (exceeding 4%), coinciding with favorable gold returns.[1] This particular phase spanned from the fourth quarter of 2007 to the second quarter of 2008, which notably occurred during the depths of the Global Financial Crisis (GFC). Despite the favorable performance of gold during this period, it’s intriguing to observe that inflation or inflation expectations didn’t seem to be significant driving forces. Further, between 1980 and 1984, the average annual inflation rate stood at 6.5%, yet gold prices experienced an average decline of 10% each year.[9] Similarly, during the period spanning from 1988 to 1991, despite an average annual inflation rate of approximately 4.6%, gold prices saw an average yearly decrease of around 7.6%.[9]

Investors can buy physical gold bars or coins, invest in gold ETFs (Exchange Traded Funds) that track the price of gold, or purchase shares in gold mining companies. However, gold offers no income and requires careful storage considerations. These forms of investment can be part of a diversified portfolio that includes bond investments and other assets to mitigate risk and secure retirement savings.

Commodities: A Basket of Inflationary Assets

Commodities encompass a broad array of raw materials crucial to various industries, including oil, grains, and metals. The prices of these commodities are typically influenced by the intricate interplay of supply and demand dynamics within the market. Notably, fluctuations in inflation often exert significant pressure on commodity prices, as rising inflation tends to escalate the costs associated with production and transportation. Consequently, this inflation-induced upward pressure often translates into higher prices for commodities, making them an attractive option for investors seeking a hedge against inflationary pressures and aiming to boost investment returns. This is particularly evident in the case of agricultural commodities and energy products, where price movements can be particularly sensitive to inflationary trends.

Commodities exhibit unique behaviors distinct from traditional asset classes, particularly in response to unforeseen shifts in supply that can trigger price shocks. For instance, events such as the disruption in wheat and oil supply following the Russian invasion of Ukraine or prolonged factory closures in China due to a stringent zero-COVID policy can significantly impact commodity prices. Vanguard’s research indicates that commodities have demonstrated an inflation beta ranging between 6 and 9 over the past three decades, surpassing that of all other asset classes analyzed. This implies that a 1% increase in unexpected inflation could lead to a 6% to 9% escalation in commodity prices. Further, drawing from past performance data, it appears justifiable to anticipate that a diversified portfolio comprising collateralized commodity futures could potentially yield an annualized long-term risk premium of approximately 3%, enhancing investment returns and contributing to risk mitigation. Consequently, even a modest yet strategically positioned allocation to commodities can serve as a potent hedge within an investment portfolio, providing an amplified safeguard against inflationary pressures, and can be integral to securing retirement savings.

Real Estate: A Tangible Hedge with Income

Investing in real estate, especially income-generating properties such as apartments or commercial buildings, offers a potential shield against inflation. With inflationary pressures, rental incomes often rise in tandem, offering investors a built-in defense against escalating costs and enhancing investment returns. Furthermore, the inherent appreciation in the value of the property over time serves as an additional safeguard, contributing to retirement savings. Nevertheless, it’s crucial to acknowledge that real estate investment demands substantial initial capital, continuous upkeep expenses, and may lack the liquidity of other investment options such as bond investments.

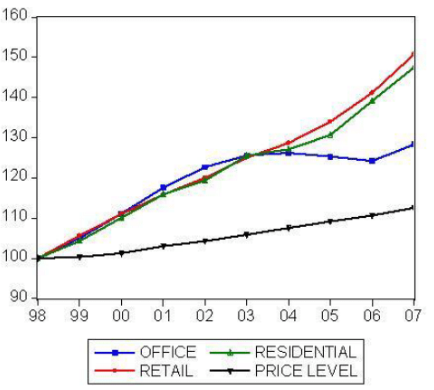

Fig 2- Price v/s Real Estate returns[4]

The visual represented above illustrates the progression over time of the German consumer price index, with the base year set at 1998 (indexed at 100), alongside the IPD total return indices for office, retail, and residential properties over the same period, also referenced against the base year of 1998 (indexed at 100). This depiction allows for a comparative analysis of the trends in consumer price inflation and the total returns generated by different sectors of the property market spanning the years from 1998 to 2007.

Stocks: A Long-Term Play with Inflationary Potential

Stocks embody ownership stakes in corporations, granting shareholders rights and potential profits from the company’s performance. Historically, stocks have demonstrated the ability to outpace the rate of inflation over extended periods, thereby contributing significantly to investment returns and retirement savings. As per a study, equities outperform inflation 90% of the time when inflation is rising and at lower levels.[6] This trend is often attributed to companies adjusting prices to mitigate the effects of inflation, thereby potentially bolstering profits and consequently driving stock prices higher, sometimes resulting in increased dividend payouts to shareholders. This could be an effective risk mitigation strategy to safeguard the portfolio against inflation.

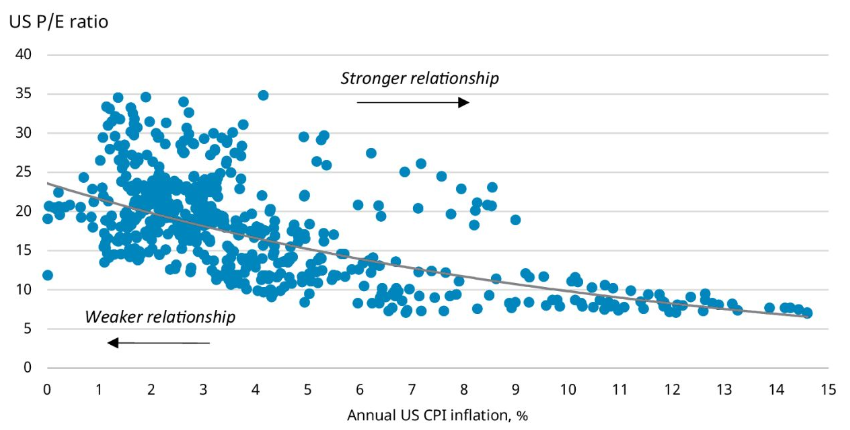

Fig 3 – CPI v/s US P/E Ratios[6]

As per the illustration above, with rising CPI index values, the overall Price-to-Earnings ratio tends to decrease, offering protection against inflation. However, it’s crucial to recognize that stock prices are subject to a myriad of influences beyond inflation dynamics, and their short-term fluctuations can be notably volatile. Various market forces, economic conditions, and company-specific factors can impact stock prices, making investment in stocks a dynamic and multifaceted endeavor. This is evident by the fact that despite occasional downturns, the stock market has consistently produced returns that surpass inflation, as over the course of the last 95 years, the average annual returns of the stock market have amounted to 12.3%.[7] Including stocks in a diversified portfolio that also features bond investments can further enhance these benefits, providing a robust framework for long-term financial growth.

TIPS: Tailored Protection from Uncle Sam

Treasury Inflation-Protected Securities (TIPS) represent bonds issued by the U.S. government, designed to maintain pace with inflation by adjusting their principal value. Consequently, the interest payments tied to TIPS are calculated based on this adjusted principal amount, safeguarding investors against the erosive effects of inflation and ensuring their returns mirror the changing cost of living, thus supporting investment returns and retirement savings.

Every year, the U.S. Treasury modifies the par value of bonds in accordance with the consumer price index, which serves as a gauge of inflation. Conventional bonds typically uphold fixed par values, making them susceptible to depreciation over time due to inflationary gains. Linking the bond’s value to inflation through indexing offers a safeguard against the erosion of purchasing power for investors, representing a crucial risk mitigation strategy. Regardless of fluctuations in prices throughout the duration of your Treasury Inflation-Protected Securities (TIPS) investment, your initial investment retains its purchasing power, augmented by accrued interest payments. Moreover, interest payments undergo inflation adjustments annually. While the interest rate remains consistent throughout the TIPS investment period, the semiannual interest payment correlates with the current par value of your TIPS, effectively increasing in alignment with the Consumer Price Index (CPI).

While TIPS present an attractive option for investors seeking to mitigate inflation risk with minimal volatility and a low level of risk, it’s important to note that they often yield lower returns compared to alternative asset classes. When conventional bonds offer a yield of 3% and the inflation rate stands at 2%, the interest on TIPS would amount to only 0.5%. Consequently, the effective annual return on TIPS would be approximately 2.5%.[8] In such a case, TIPS might be perceived as a less favorable option compared to non-TIPS Treasury bonds. Conversely, if non-TIPS bonds yield a meager 2%, investing in TIPS would provide an additional half a percent return over traditional bonds, enhancing the overall investment returns of the portfolio.

Research indicates that since the mid-1990s, the average break-even point has hovered around 2.5%. This implies that for a non-TIPS bond to potentially outperform TIPS, it would need to yield at least 2.5%.[8]

Portfolio Management

A traditional investment portfolio, typically composed of 60% stocks and 40% bond investments, has historically demonstrated resilience against inflation over extended periods, supporting both investment returns and retirement savings. However, in the short term, it exhibits a relatively low sensitivity to inflation, represented by a beta of 0.07. Should an investor aim to align their portfolio’s sensitivity to inflation (inflation beta) with the broader market, maintaining a value of 1.00, adjustments to the asset allocation become necessary. One approach involves integrating commodities into the portfolio, constituting approximately 12% of the total allocation, alongside a smaller portion dedicated to Treasury Inflation-Protected Securities (TIPS), with 2% allocated specifically (1% each for short-term and intermediate-term TIPS), enhancing risk mitigation strategies.

Conversely, commodities present a distinct investment proposition characterized by a lower average correlation of 0.34 with traditional asset classes. However, they exhibit a notably higher inflation beta of 7.60, indicating a more pronounced responsiveness to inflationary movements. This implies that for every 1% change in inflation, commodity prices, on average, tend to adjust by approximately 7.6%. Consequently, commodities serve not only to hedge against inflation within their own asset class but also contribute to bolstering the entire portfolio’s resilience against inflationary pressures, thereby protecting investment returns and retirement savings in a diversified investment strategy.

Conclusion

In conclusion, safeguarding your investments from the corrosive effects of inflation is crucial for long-term financial well-being. While no single asset class provides a perfect solution, a well-diversified portfolio that incorporates various inflation hedges can offer robust protection. Gold, with its historical stability and scarcity, serves as a time-honored safe haven. Commodities, with their sensitivity to supply and demand dynamics, can provide amplified returns during inflationary periods. Real estate investments, particularly income-generating properties, offer a tangible hedge with the potential for rental income growth. Stocks, while volatile in the short term, have demonstrated an ability to outpace inflation over extended periods. Treasury Inflation-Protected Securities (TIPS) offer a government-backed solution, directly linking returns to changes in the cost of living. By strategically allocating investments across these asset classes, investors can construct a resilient portfolio equipped to withstand the challenges posed by rising inflation. Ultimately, proactive portfolio management and a diversified approach remain crucial in navigating the ever-evolving economic landscape and preserving the purchasing power of hard-earned savings.

References

[1] “Investment Update – beyond CPI: Gold as a Strategic Inflation Hedge.” n.d. World Gold Council. https://www.gold.org/goldhub/research/beyond-cpi-gold-as-a-strategic-inflation-hedge.

[2] “The Inflation-Fighting Power of Commodities.” n.d. Corporate.vanguard.com. https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/inflation-fighting-power-of-commodities.html.

[3] “Commodities Offer Hedge against Inflation.” n.d. London Business School. https://www.london.edu/news/commodities-offer-hedge-against-inflation-2153.

[4] Demary, Markus & Voigtländer, Michael. (2009). The Inflation Hedging Properties of Real Estate: A Comparison between Direct Investments and Equity Returns.

[5] “Hedging Your Portfolio against Inflation.” n.d. Corporate.vanguard.com. https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/hedging-portfolio-against-inflation.html.

[6] “Which Equity Sectors Can Combat Higher Inflation?” 2022. Hartford Funds. February 9, 2022. https://www.hartfordfunds.com/insights/market-perspectives/equity/which-equity-sectors-can-combat-higher-inflation.html.

[7] Tretina, Kat. 2023. “How to Hedge against Inflation – Forbes Advisor.” Www.forbes.com. March 21, 2023. https://www.forbes.com/advisor/investing/how-to-hedge-against-inflation/.

[8] O’Connell, Brian. 2021. “Treasury Inflation Protected Securities (TIPS).” Forbes Advisor. April 13, 2021. https://www.forbes.com/advisor/investing/treasury-inflation-protected-securities-tips/.

[9] Duggan, Wayne. 2022. “Is Gold an Inflation Hedge?” Forbes Advisor. August 17, 2022. https://www.forbes.com/advisor/investing/gold-inflation-hedge/